Engineering Your Lending CMS

In our Reimagine Your Workplace series, we’ve explored the strategic advantage for lenders to integrate a hybrid approach to operating. We touched upon the people, processes, and technology. However, perhaps the most foundational element of all is your Compliance Management System (CMS). CMS cannot be a reactive measure; lenders must engineer their CMS with an intentional plan and a proactive approach to compliance.

CMS Examinations

Examiners must review CMS during every supervisory cycle to complete the consumer compliance core assessment and assign the consumer compliance component rating.

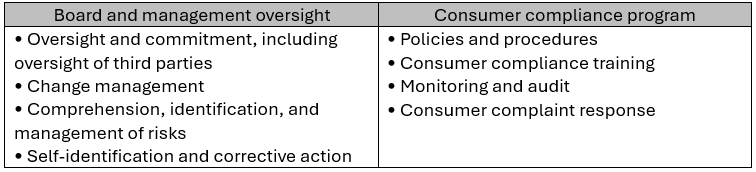

An effective CMS is commonly comprised of two interdependent elements[1]:

Board and management oversight; and

Consumer compliance program

The following table outlines broadly what examiners consider when assessing board and management oversight and the compliance program, respectively:

The complexity of the compliance risk environment presents challenges for regulated institutions. The volume and complexity of consumer protection-related laws and regulations coupled with changing technologies and earnings pressures increase the importance of an institution’s CMS. Each entity should develop and maintain an effective CMS that is appropriate for the size, complexity, and risk profile of its operations.

Management should comprehend, identify, and manage consumer compliance risks, including existing and emerging risks to the institution’s products, services, and other activities. The sophistication of risk management should be proportionate to the present risks and the institution’s size and complexity.

Regardless of the size and complexity, sound management of consumer compliance risk should Identify, Measure, Monitor, and Control Compliance Risk.

Completing risk assessments helps management identify current and emerging consumer compliance risks in order to prevent, self-identify, and address potential consumer compliance issues. A well designed risk assessment process should be supported by appropriate methodology that includes quantitative and qualitative data and evaluates risk across all products, services, and lines of business. An effective risk assessment process helps the board and management address emerging risks at an early stage and allows them to proactively develop and implement appropriate strategies to mitigate the risks before the risks have an adverse effect on the institution’s condition or risk profile.

Self-Identification and Corrective Action

Management should identify, respond to, and remediate violations of laws or regulations and deficient practices in a timely manner. Moreover, self-identification and prompt correction of violations and deficient practices may reflect strengths in the bank’s CMS and could indicate management’s and the board’s commitment to address responsibly underlying consumer compliance risk. Appropriate corrective action should remedy harmed parties, correct programmatic weaknesses related to the violation, and prevent violations from occurring in the future.

Intentional Design: The Cornerstone of Proactive Compliance

Engineering your CMS intentionally starts with a comprehensive understanding of the regulatory landscape. Lenders should:

Conduct Proactive Risk Assessments: Regularly assess potential compliance risks, not just in response to changes, but as a continuous process. Identify vulnerabilities and design controls before they become issues.

Design for Scalability and Adaptability: The regulatory landscape is dynamic. Your CMS should be engineered to adapt to new rules and scale with your institution's growth. Avoid rigid systems that require costly overhauls with every change.

Centralize Data and Reporting: An intentional CMS design includes a centralized data repository for all compliance-related information. This allows for efficient monitoring, reporting, and analysis, providing a holistic view of your compliance posture.

Culture of Compliance: The Human Element

Even the most sophisticated CMS will fall short without a strong culture of compliance. Engineering an intentional approach includes fostering an environment where compliance is everyone's responsibility. This involves:

Comprehensive Training and Awareness Programs: Regularly educate employees on relevant regulations and their role in maintaining compliance. Make training engaging and relevant to their specific functions.

Automate Key Compliance Processes: Leverage technology or an outsourced partner to automate repetitive or high-risk compliance tasks. Monitor the outputs of these regular reviews and use them as the cornerstone for change initiatives.

Moving Forward with Intention

At SCA, we understand the intricacies of the lending compliance landscape and that no two compliance management systems are alike. We are equipped to be your strategic partner in building and maintaining a robust CMS tailored to your institution’s specific risk profile to ensure satisfactory exam ratings. Whether you need to empower your existing team or supplement it with our expertise, SCA offers a range of services to support your compliance goals. Our experienced professionals can step in and serve as interim compliance officers, or work alongside an existing team, providing the leadership and expertise needed to navigate complex regulatory requirements.

For more information, contact our Director, Bill Dolan, at wdolan@scapartnering.com or by phone at (617) 694 -2617 and see how SCA can help transform your CMS today!

[1] FDIC Consumer Compliance Examination Manual II-3.1